Preparing for Retirement

Wherever you are in your journey through life, every goal begins with a solid plan — and retirement is no exception. As Mark Twain wisely said, “Twenty years from now, you will be more disappointed by the things you didn’t do than by the ones that you did do.”

It’s YOUR Journey

Starting your career is an exciting yet overwhelming time filled with possibilities. As you embark on this journey, it’s essential to develop the skills and financial habits that will support you throughout your life.

Before you can plan effectively, take a moment to define your dreams and priorities. Do you envision:

- Starting a family?

- Furthering your education?

- Traveling the world?

- Pursuing a passion project?

- Spending quality time with loved ones?

- Giving back to your community?

These aspirations will form the foundation of your journey and guide your financial planning.

Start with a Vision

Just like building a house requires a blueprint, planning for your future needs a clear vision. Here’s why it matters:

- Clarity: A defined destination makes your path smoother.

- Motivation: Your ‘why’ keeps you focused and inspired.

- Personalization: Your plan should evolve with your experiences and interests.

Effective planning today can lead to a comfortable future, allowing you to pursue what you love without stress. Even small changes can make a significant impact over time. Leveraging the tools and resources offered by ZOLL Benefits can start you on your way to success.

Manage Your Finances

Does Anyone Like the Word Budget?

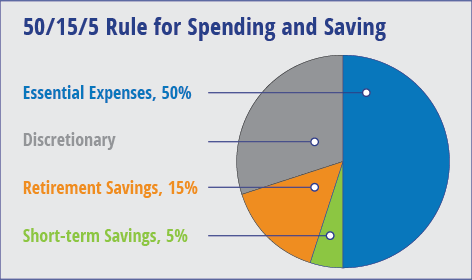

Creating a budget is a crucial step toward financial stability and achieving your long-term goals. While the word “budget” might not excite everyone, having a plan for your money can reduce stress, help you avoid debt, and set you up for future success. But what if we could make budgeting feel less restrictive and more empowering? After significant research, Fidelity developed the 50/15/5 rule — a simple guideline for saving and spending that can help you take control of your finances:

- Aim to allocate no more than 50% of your take-home pay to essential expenses.

- Save 15% of your pretax income for retirement.

- Keep 5% of your take-home pay for short-term savings.

While your personal situation may differ, this framework offers a solid starting point for managing your money effectively. By following this guideline, you can ensure you’re covering your needs, preparing for the future, and still have room for flexibility in your spending.

- Click here for an interactive budget worksheet from Fidelity.

- Explore the Fidelity Savings and spending check-up to see where you stand on the 50/15/5 rule.

Essential Expenses: 50%

Some expenses simply aren’t optional — you need to eat, and you need a place to live. Consider allocating no more than 50% of take-home pay to “must-have” expenses, such as:

- Housing – mortgage, rent, property tax, utilities (electricity, etc.), homeowners/renters’ insurance, and condo/home association fees.

- Food – groceries only; do not include takeout or restaurant meals, unless you really consider them essential, i.e., you never cook and always eat out.

- Health care – out-of-pocket expenses (e.g., prescriptions, copayments).

- Transportation – car loan/lease, gas, car insurance, parking, tolls, maintenance, and commuter fares.

- Childcare – day care, tuition, and fees.

- Debt payments and other obligations — credit card payments, student loan payments, child support, alimony, and life insurance.

Establish a Plan for Repaying Debt

If you’ve accumulated student loans or credit card debt, especially due to high tuition costs, it’s important to establish a repayment plan as part of your overall budget. Consider these approaches to pay off your debt faster:

- Debt Consolidation: Combine multiple debts into a single loan, potentially with a lower interest rate.

- Accelerated Repayment: Make larger or extra payments toward the principal when possible.

- Prioritize High-Interest Debt: Focus on paying off debts with the highest interest rates first.

- Budget for Debt Repayment: Allocate a specific portion of your income to debt reduction each month.

By implementing a structured plan, you can work toward becoming debt-free more quickly and efficiently.

Keep it Below 50%:

Just because some expenses are essential doesn’t mean they can’t be adjusted. Small changes can make a big difference. Consider simple tweaks like:

- Lowering your thermostat a few degrees in winter and raising it in summer.

- Buying groceries on sale and stocking up.

- Opting for frozen fruits and vegetables instead of fresh.

- Packing your lunch for work.

These minor adjustments can add up over time.

Retirement Savings: 15%:

It’s important to save for your future — at every age. Here’s why:

- Social Security alone is unlikely to fully fund the retirement lifestyle most people envision. Fidelity estimates suggest that about 45% of retirement income will need to come from personal savings.

- Consider saving 15% of your pretax household income for retirement. This includes both your contributions to your 401(k) and any employer matching funds.

- The keys to building a robust retirement fund are:

- Start early.

- Save consistently.

- Invest wisely.

- Maximize your savings potential by utilizing tax-advantaged retirement accounts such as 401(k)s, 403(b)s, or IRAs.

Remember, it’s never too early or too late to start planning for your financial future. The sooner you begin, the more time your money has to grow.

How to Get to 15%:

Saving 15% of your income for retirement might seem challenging at first, but there are strategies to help you reach this goal:

- Gradual Increase: ZOLL’s 401(k) Savings Plan offers a program that allows you to automatically increase your contributions annually until you reach your target savings rate. This allows you to start small and build up over time.

- Maximize Employer Match: Begin by contributing at least enough to take full advantage of your employer’s matching program. This is free money for your retirement. ZOLL offers up to 5.5% in matching contributions (100% of the first 4% and 50% of the next 3%).

- Leverage Raises and Bonuses: When you receive a salary increase or bonus, consider directing some or all these extra funds into your retirement accounts. This can help you boost your savings without feeling a pinch in your regular budget.

- Aim for Contribution Limits: As your savings ability grows, work toward maxing out your annual contribution limits for workplace savings plans or individual retirement accounts.

Remember, every step toward saving, no matter how small, is progress toward a more secure financial future.

Short-term Savings: 5%

Short-term savings, also known as emergency savings, are necessary for everyone. Life’s unexpected events — like illness or job loss — can be stressful enough without the added burden of financial strain. Start by setting aside $1,000, then gradually build up to cover three to six months of essential expenses such as housing, food, and utilities. Treat emergency savings like a monthly bill until you’ve reached your goal.

Plan for smaller surprises, too. In addition to major emergencies, it’s helpful to save a portion of your income for smaller unplanned expenses. Think wedding invitations, cracked phone screens, flat tires, or overlooked costs like car maintenance, kids’ field trips, doctor copays, and holiday gifts.

How to Get to 5%:

Make saving automatic. Setting up automatic transfers from your paycheck to a separate account dedicated to short-term savings can help you reach your goal of saving 5% of your income for life’s everyday surprises.

Start Now, Thank Yourself Later: Why Retirement Planning Matters Today

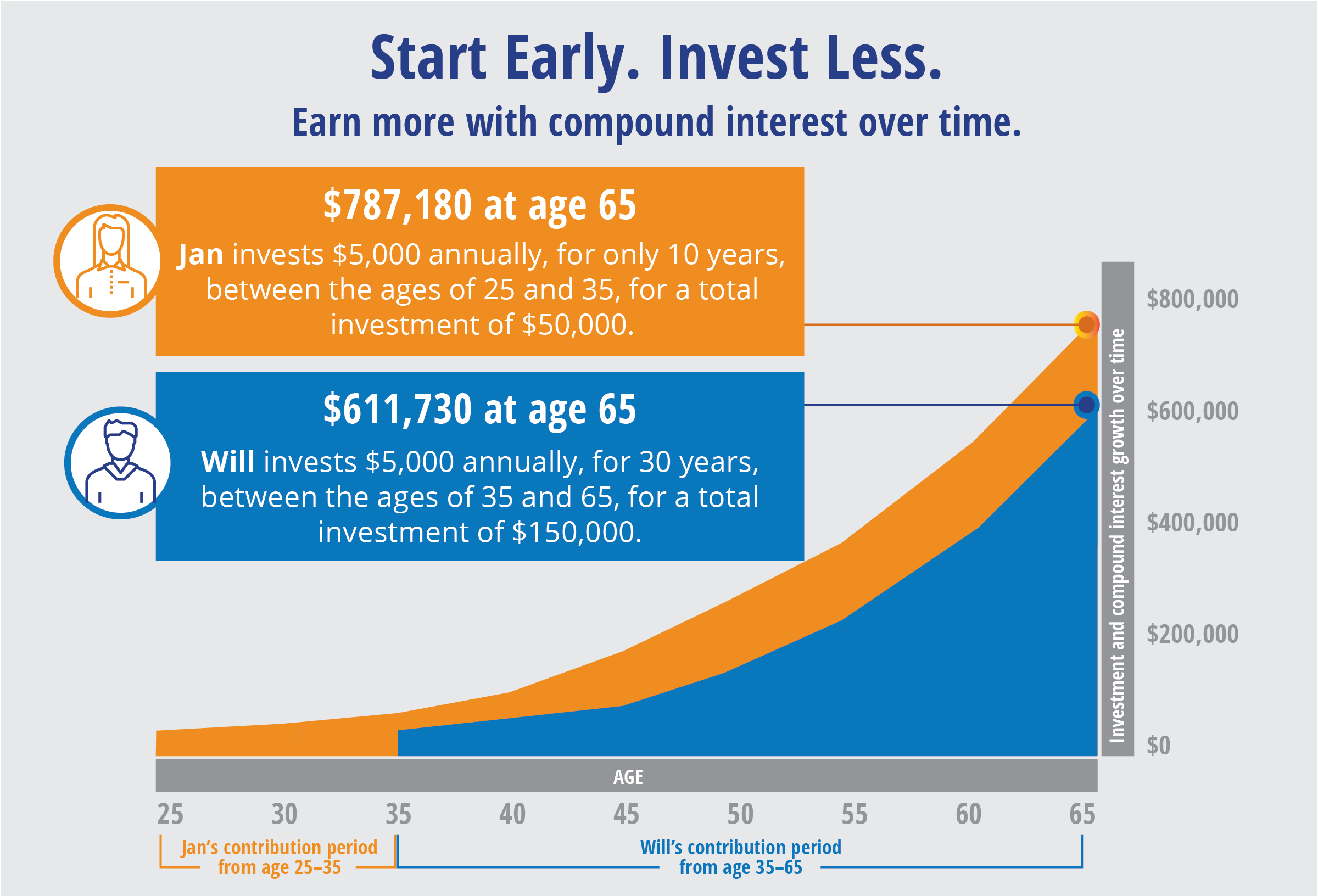

Retirement might feel like a lifetime away, but starting early is one of the smartest financial moves you can make. The earlier you begin saving, the more time your money has to grow — and that is where the magic of compounding interest comes in. Even small contributions now can turn into significant savings down the road.

What is Compound Interest?

Compound interest is like a snowball effect for your money. Over time, compound interest can make your money grow much faster than simple interest (which only calculates interest on the original amount).

Here’s how it works:

- Initial savings: Imagine you put some money in a savings account that earns interest.

- First round of interest: After a certain period (say, a year), you earn interest on that initial amount.

- The “compound” part: The next time interest is calculated you earn it on Your original money PLUS the interest you already earned.

- It keeps growing: This process repeats, so you’re constantly earning interest on a larger and larger amount.

NOTES: Example assumes an 8% interest rate, compounded annually. Balances are approximate.

KEY TAKEAWAY:

Starting early means contributing less but saving more over time with compound interest.

- Jan started saving earlier, contributing for only 10 years. She has more saved at age 65 than Will.

- Will started saving later and contributed for a longer period, 30 years until he reached retirement age. He still has less saved at age 65 than Jan.

Remember: Compound interest can work for you (in savings) or against you (in debt), so it’s important to understand how it functions!

Take Advantage of Employer Sponsored Retirement Plans

If your employer offers a 401(k) or similar retirement plan, take advantage of it — especially if they provide matching contributions. That is free money for your future! Make saving for retirement a regular habit, even if it feels far off — it will make a huge difference down the road. ZOLL sponsors a 401(k) Savings Plan through Fidelity to help you build a strong financial foundation for your retirement and matches up to 5.5% (100% of the first 4% and 50% of the next 3%).

Make Saving a Regular Habit

Saving for retirement doesn’t have to be overwhelming. Start by making it a regular habit, even if it’s just a small amount. The key is consistency. By beginning now, you’re setting yourself up for financial freedom and peace of mind later in life. Your future self will thank you!

Manage Your Investment

Ensuring your investments are on track is vital for a brighter tomorrow. ZOLL partners with CAPTRUST Financial Advisors to provide expert guidance at every stage of your journey, helping you plan with confidence.

- Schedule your FREE one-on-one call with a CAPTRUST advisor to:

- Create your personalized financial blueprint.

- Find the investment strategies that align with your risk tolerance and time horizon.

- Craft a diversified, tax-smart portfolio personalized for you.

- Regularly review your investments with your advisor to ensure you’re staying on track to meet your goals.

- Set a schedule (e.g., quarterly or annually) to evaluate your progress and adjust as needed. Changes in market conditions, new legislation, personal circumstances, or shifting priorities may require updates to your plan over time.

Journeys are not always easy — there will be times when you feel like giving up, when life knocks you down or takes you by surprise. But the true test is to keep moving forward, staying resilient through every challenge.

Maintain Your Physical Fitness

In your 20s and 30s, your body is at its peak in terms of strength, endurance, and recovery. And although you may think you are in great shape with not a care in the world, this is the ideal time to build habits that will set the stage for lifelong health.

Regular Check-ups and Screenings

Annual physical exams are essential for preventive care and early detection of potential health issues. All ZOLL medical plans include free in-network preventive care and prescription drug coverage through OptumRx to support your best health.

These regular check-ups allow your doctors to:

- Monitor changes in your health over time.

- Assess potential health risks based on family history.

- Provide personalized advice for maintaining a healthy lifestyle.

- Perform necessary preventive screenings for conditions like high cholesterol, diabetes, and certain cancers.

In addition, consider these proactive tips to prevent or delay the onset of various health conditions:

- Stay up to date with vaccinations.

- Maintain a healthy weight.

- Limit alcohol consumption.

- Avoid smoking or tobacco products.

- Protect your skin from sun damage.

By prioritizing your health today, you’re laying a strong foundation for better health in your later years.

Establish Healthy Habits

Your lifestyle choices during these years can significantly impact your long-term health. Focus on:

- Developing a consistent exercise routine.

- Adopting a balanced, nutritious diet and staying hydrated.

- Managing stress effectively.

- Ensuring adequate sleep to lessen your risk of serious health conditions and improve your overall well-being.

Remember, the habits and choices you make now can have a lasting impact on your future well-being. By combining the proactive benefits of annual checkups with the personalized support of health professionals like coaches and nutritionists, you can build a strong foundation for a healthier future.

ZOLL offers free support through Healthy Hearts! Healthy You! and Modern Health. Review the support resources at the bottom of the page.

ZOLL’s medical plans offer fitness, weight loss membership, and gym reimbursements through UnitedHealthcare and Aetna. Check them out here. Additionally, some ZOLL locations offer onsite fitness facilities. Speak to your HR Benefit Advocate to learn more.

Balance Life After Work

Navigate Your Emotional Journey

Find Support When You Need it

NEED MORE INFORMATION ON THIS BENEFIT?

Refer to the quick links buttons to the right.